In our earlier article ‘The Buy Now, Pay Later Revolution’, we discussed the explosion of the Buy Now, Pay Later (BNPL) sector and how the popularity of BNPL will make some of the largest gains out of all payment methods *nearly doubling its share by 2024 to account for 13.6% of e-com spend.

As BNPL levels of growth are only set to increase, banks should take note of the growth that is anticipated in the next generation of consumers.

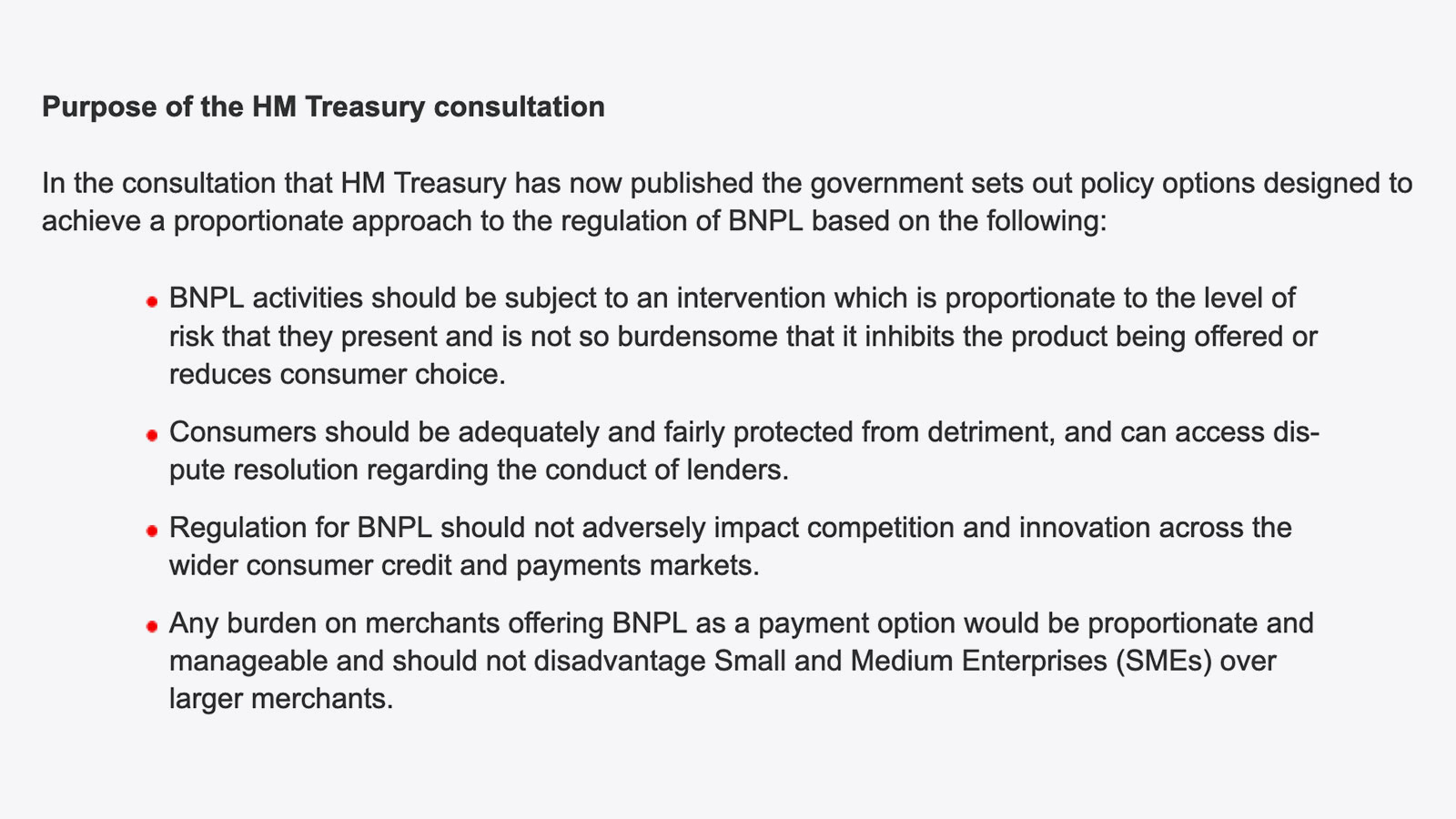

Consumer protection and more

In the financial services industry - one of the most heavily regulated industries in the world, short-term credit such as BNPL that is used to finance the purchase of goods and services has long been exempt from regulation. However, this is now all about to change…

BNPL goods, like typical credit card products, let customers purchase a good or service immediately, and pay later. How BNPL differs is that payments are made in equal instalments over a predetermined length of time, usually up to 4 months, with no interest payable as long as payments are made on time. However, missing or skipping a payment may mean late fees and penalties, or high interest rates. Falling behind on one or more payments can reflect negatively on the customer's credit score.

So, BNPL’s regulatory challenge extends beyond simply ensuring that consumers are aware of any hidden fees or risks associated with the new type of credit. Instead, the concern is whether the EU regulatory framework is effective in moulding the new normal that is emerging.

In this regard, the United Kingdom may be the first country to enact new regulations for BNPL in 2022, bringing legal certainty to companies and more protection to consumers.

Source: Norton Rose Fulbright

Buy Now, Pay Later regulation is needed in order to provide proportionate consumer protection. It will allow clarity and consistency for customers, retailers and BNPL providers as well as ‘defining’ BNPL in legislation.

Redefining the Payment Landscape

BNPL providers are redefining the banking landscape. The merchant, not the consumer, is charged for access to BNPL under this business model. The approach is designed to provide businesses with a payment mechanism that boosts revenue by allowing customers to control their payments over time. Basket conversion rates have increased phenomenally, including the overall value of a basket (as well as customer loyalty), meaning that these values are persuasive enough for a merchant to subscribe to a provider for a monthly fee and a % transaction.

Developing these partnerships with merchants that are focused on increasing revenue, also prompts new product innovation.

Merchant cash flow. Revenue generation, One-stop shop for consumer personal finance management. Creation of cross-audience services that connect the consumer and merchant in more engaging relationships and empower the merchant with data and the ability to drive offers, reward points as well as ongoing business decisions. Customer loyalty. Customer experience and satisfaction. Uplifts in order value and increased basket conversion rates. These are all some of the benefits that go hand in hand with BNPL.

A changing attitude towards credit

BNPL has been stereotyped as a solution for people who live from payday to payday, however research carried out by multiple sources have identified that this is in fact a perfect solution for budget conscious and ‘credit averse’ customers. It also provides individuals with the flexibility to manage their finances, regardless of their income level. Contrary to the youthful marketing image that BNPL portrays, the biggest users of BNPL* are in fact 35 - 44 year olds, followed by over 65s. 48% of BNPL users will not buy from a merchant if they do not offer a BNPL option**.

BNPL usage is highest in the 25-44 age groups, but it also is meaningful among 45-to-54-year-old

Source: Capco.com / Bain & Company survey of 2,002 UK consumers who shopped online in the past 12 months, conducted July 2021

More and more consumers embrace the ease and convenience of BNPL whilst retailers benefit from higher conversion rates.

BNPL thrives off consumers’ desire for more transactional convenience rather than the need for an alternative source of credit. Our earlier article, ‘The Buy Now, Pay Later Revolution’ explained how debit card spending accounted for 68.8% of all cards issued in Europe and how debit cards outstrip credit cards by a ratio of 2.21 to 1. Spending on debit cards has been growing at a compound rate of 13.17 percent over the last five years – more than twice the rate at which debit cards have been issued – demonstrating the popularity of the debit function.

The Point of Sale (POS) segment boom

The POS financing segment in particular is anticipated to grow significantly. Many businesses around the world are focussing on providing POS BNPL options to improve customer experience and strengthen customer relationships. Furthermore, businesses provide customers with transparent, loyalty-driven POS instalment funding options. As a result, businesses can expect to experience a higher proportion of repeat customers.

Although POS financing has been around for years (banks have been partnering with merchants for decades), which in turn have benefited banks, merchants and customers in the form of co-branded credit cards. However, fintechs have recognized that customers have been transitioning to the subscription model and mindset of BNPL and debit cards. In turn, the number of fintech companies offering direct-to-consumer financing has increased dramatically.

The credit overhaul - BNPL leads the way - Banks need to adopt or be left behind

The growth of BNPL services highlights the necessity for banks and credit card companies to respond rapidly to this demand for change. Banks have always been considered a trusted source of lending and therefore, it makes sense to offer their customers a choice in paying by interest-free instalments. Banks including Barclays, Monzo and Revolut have shown interest and are offering similar services.

When customers are made aware that payment can be made in the form of BNPL, usage is high. Users in the U.K alone saved 103 million pounds in credit card interest costs in 2020. Furthermore, even if payments are missed, cost savings are still cheaper in comparison to credit cards. The following (BNPL vs credit cards) comparison from Bain & Company Inc details the comparison of fees and interest on a single £75 purchase:

Illustrative comparison of fees and interest on a single £75 purchase (£)

Source: Bain & Company Inc

So, BNPL is more than a passing fad; allowing consumers to pay in equal instalments over an agreed period is the fastest growing segment of finance. Consumers like BNPL, they like the transparency, the predictive payments as well as budgeting against those payments.

Banks will win in BNPL by combining data-driven consumer intelligence with personalized solutions. There are multiple business models that banks can use to enter the BNPL market ranging from providing a BNPL company with funding capacity, partnering with BNPL(s), integrating instalments into credit cards or even acquiring a BNPL company.

Banks have an inherent advantage- existing high levels of customer trust. Furthermore, banks are heavily regulated, have vast amounts of data that goes beyond a credit score that, when combined with AI and machine learning, can assist them in making effective decisions on BNPL.

Banks may leverage these benefits by focusing on the customer experience and harnessing the power of open, cloud-based banking solutions. BNPL offers an abundance of possibilities and opportunities and therefore, banks need to start looking beyond credit cards, leveraging their own strengths by focusing on new ways to add value for consumers and merchants. Though banks may be late in catching up, they have the potential to regain market share for a number of reasons;

- Access to technology

- Existing merchant relationships

- Cost of funds advantage

- An ability to weather credit cycles

Banks must respond - by not entering the market with a BNPL offering, banks may be missing out on one of the largest and explosive acquisition opportunities to date.

How does a payment Hardware Security Module (HSM) protect BNPL payment transactions?

A payment HSM is a secure, tamper-resistant cryptographic processor designed specifically to protect the lifecycle of cryptographic keys and to execute encryption and decryption routines. It provides a high level of security in terms of confidentiality, integrity, and availability of cryptographic keys and any sensitive data processed. The payment industry, banks and financial services rely on payment HSMs to secure a number of functions. In particular, for BNPL payments, these functions would be:

- Verifying debit/credit card transactions by conducting host processing duties for EMV-based transactions or checking CSVs

- Supporting a crypto-API with an EMV

- Performing secure key management

- Generating encrypted card values such as Card Verification Values (CVV, CVV2, iCVV)

- Supporting host-host key/data exchange API standards.

Conclusion

If you are considering launching a BNPL initiative as part of your payment service offering, a cloud first approach may be the optimal strategy to consider. Launching a new application in the cloud can deliver the speed to market, scalability and flexibility required to meet the requirements and expectations of today’s consumers.

To complement a cloud deployment, Payment HSM as a Service can be used to protect and secure online payment transactions.

Our Payment HSM as a Service is globally accessible, cloud-based and fully managed by industry experts.

* worldpay: The Global Payments Report 2021

** PYMNTS.com Buy Now, Pay Later tracker

Further Reading: